4Q25 results: below expectations

Operating cash flow was -$5.4 million with a step up in cash burn reducing operating cash flow. Costs increased as AYA focused on submitting Silax Coronary Plaque for FDA approval (16th July 2025) andcompleting development of Silax Coronary Flow.

Having submitted SCP to the FDA, management expects costs to return to around previous levels ($1.3 - $1.5 million per month).

Cash balance: $11.3 million

Following the receipt of the second tranche of the group’s $15 million capital raise (completed in February), AYA finished June with $11.3 million in cash. Management expects to receive an R&D tax rebate of around $4.5 million before the end of the year. The cash provides a 12-month runway during which AYA should gain FDA approval for Salix Coronary Plaque and Salix Coronary Flow, leading to immediate revenue generation from the group’s existing US customers.

SAPPHIRE study progressing

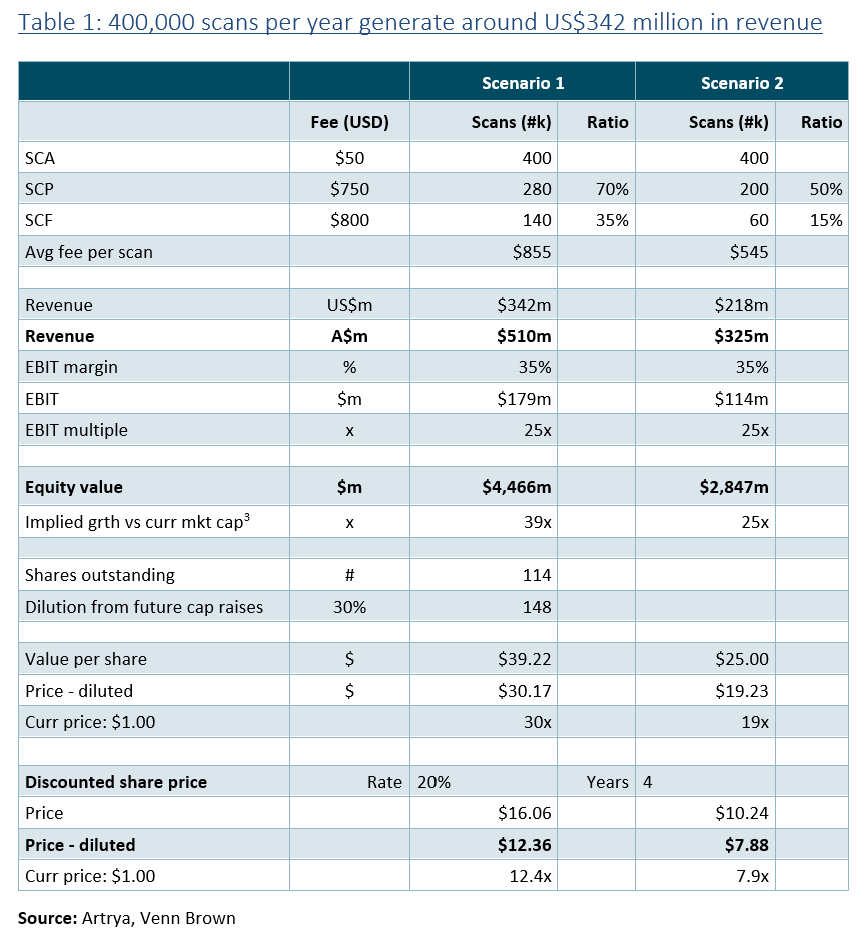

Artrya reports that it is furthering discussions with six to eight hospital groups in the US to participate in the new SAPPHIRE study. Combined, these groups perform approximately 400,000 scans per year (~9% of the market), which equates to around US$342 million in revenue. While nothing has yet been agreed upon, the discussions provide some validation of Salix’s capability and the respect and interest Artrya is generating in the high-paying market.

Table 1 provides some perspective on the value of the SAPPHIRE participants. Assuming management’s pricing and scan rates (every 100 SCA analyses leads to 70 SCP and 35 SCF analyses) , these 400,000 scans would generate around US$342 million in annual revenue (A$526 million) . This compares to our $2.63 per share valuation, which is based on modelling that assumes in FY35 AYA’s US customers perform 336,000 SCA, delivering US$213 million in revenue. Our modelling also assumes lower SCP and SCF conversion rates1 and lower SCF pricing ($750 vs $800).

Table 1 shows the impact of applying AYA’s assumptions (Scenario 1) to 400,000 scans per year. Assuming a modest EBIT margin (35%) and EBIT multiple (25x) implies an equity value of $4.5 billion (39x AYA’s current market cap).

Assuming this scan rate is achieved in four years, applying a 20% discount rate and a 30% increase in shares outstanding due to future capital raises, the valuation implies a diluted per-share value of $12.36, 12.4x the current share price.

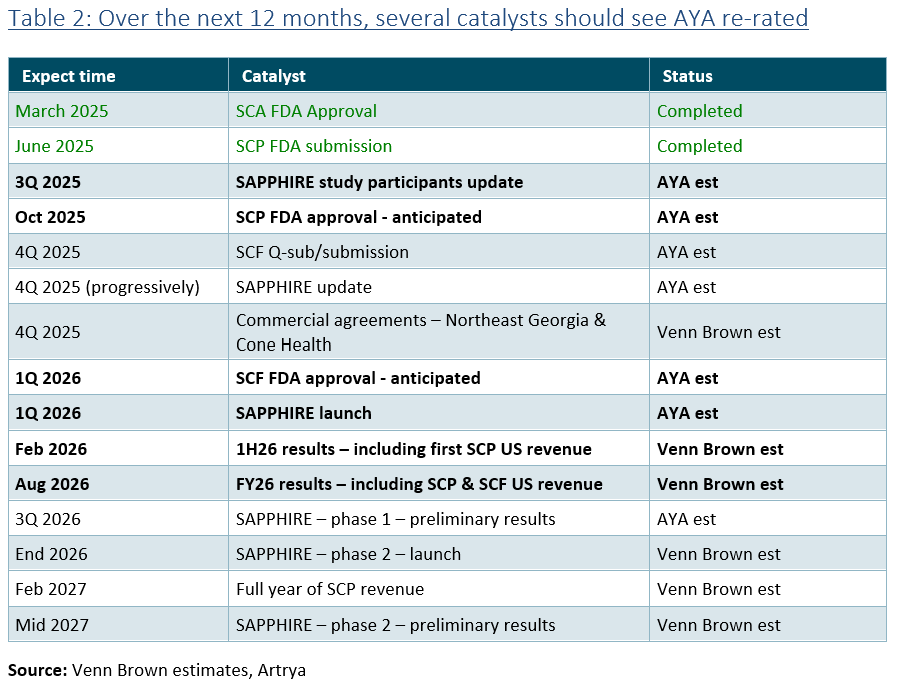

Catalysts

As discussed in our initiation of coverage report, we seeseveral catalysts that will progressively see AYA’s share price more accurately reflect the company’s fair value, including FDA approvals and commercial launch of SCP and SCF, reporting its first US revenues and the signing of SAPPHIRE study partners.

Key catalysts are: