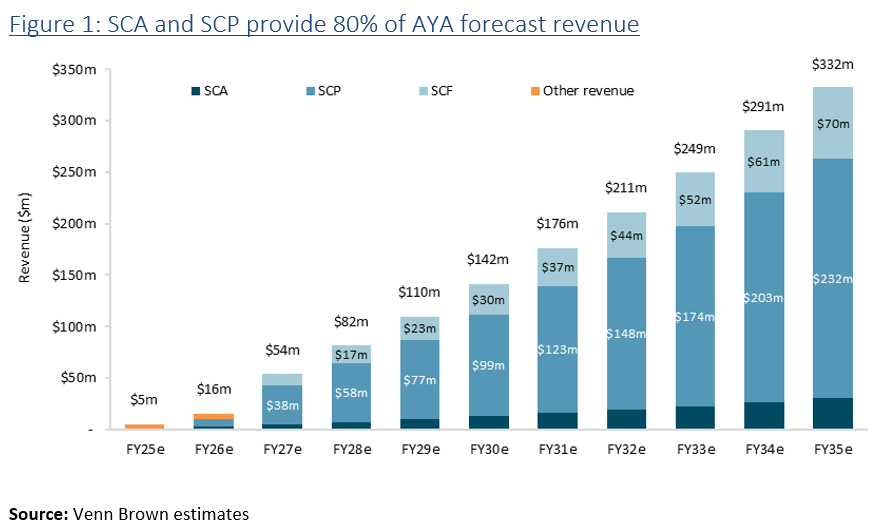

Artray announced today that its primary product, Salix Coronary Plaque (SCP) gained FDA clearance. This is a major milestone for the company, as SCP is Artrya’s core product, responsible for 70% of the group’s future revenue.

The approval means Artrya can start charging Tanner Health for SCP following the signing of a commercial agreement in July. It also means that the agreements with Artryra’s two other US partners, Northeast Georgia Health System and Cone Health, will start generating meaningful revenue.

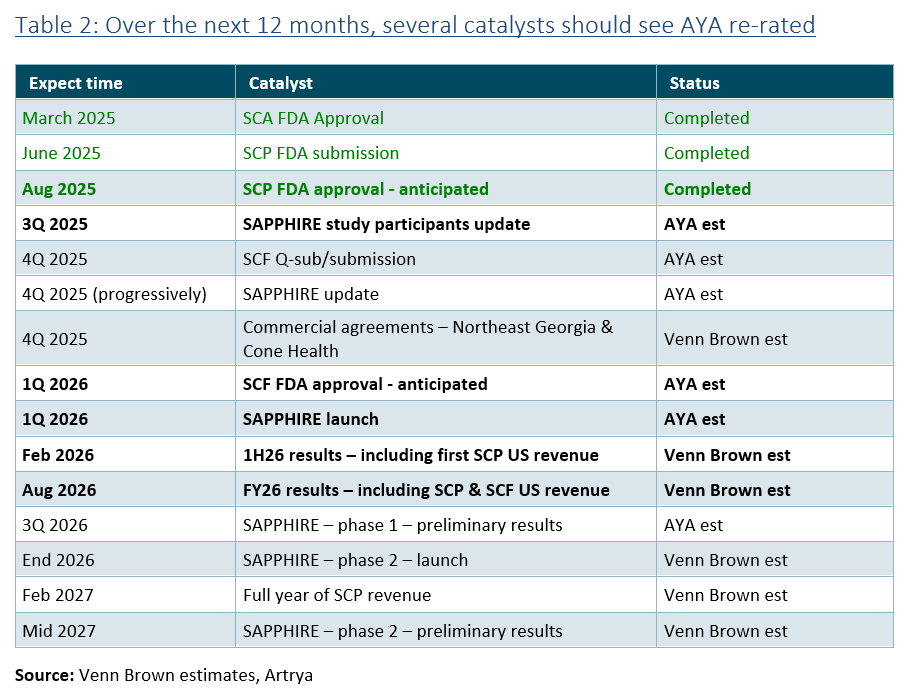

The approval of SCA (in March) and SCP leaves only Salix Coronary Flow (SCF) on the group’s current product roadmap to gain FDA approval. Like SCP, SCF will be the first coronary flow solution offering point-of-care assessment.

There is proven demand for SCF, with three companies offering solutions. However, each provides a human-in-the-loop solution with a 24-hour turnaround and without the workflow management provided by SCA. We expect SCF to contribute around 20% of the group’s revenue. AYA’s biggest competitor, the recently listed Heartflow (NASDAQGS:HTFL), has both plaque assessment and flow products on the market and has a market cap of US$2.5 billion.

FDA approval of SCP is one of the key milestones and risk factors for Artrya. With SCA and SCP approved, AYA has approval for 80% of forecast revenue, underpinning our valuation and significantly de-risking the business. We are currently reviewing our $2.63 per share valuation and will finalise it following tomorrow’s investor call.

Read more in our initiation of coverage report: ‘Salix: The future of cardiac imaging diagnostics’ and other research available on our website: www.vennbrown.com/artrya.

Artrya is hosting an investor call tomorrow (Friday) at 11:30am AEST. Register using the following link: https://artrya.zoom.us/webinar/register/WN_9ke5TnZATEGINQn6ZUq-VQ

As shown in Table 1,Artrya’s customers actually generate revenue from using SCP and SCF with the USMedicare rebates exceeding Artrya’s fee guidance (and Venn Brown’sassumptions).

The company has previously stated that FDA approval willimmediately transition commercial agreements into full fee-paying services forSCP (and later SCF). Given SCP’s US$950 per scan US Medicare rebates don’t comeinto affect until 1st January 2026, there is a chance these clauseswill be delayed until then.

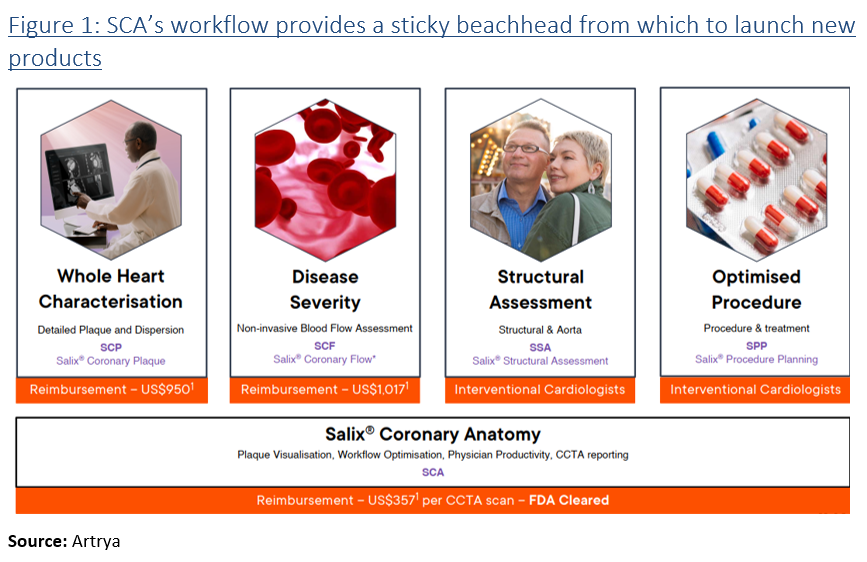

It’s worth remembering that Artrya has priced Silax Coronary Anatomy (SCA) to minimise the friction of adoption by health services, with the time and efficiency savings offered by the workflow system easily surpassing the cost.

Artrya’s other products, including SCP and SCF, are fully integrated into SCA and appear to users simply as features within the interface. SCA is an ideal launch tool for SCP and any future products. Once integrated within a health centre’s workflow, Artrya can roll out new products by simply enabling a new menu button.

The last three years have seen the values of almost all non-revenue-generating small and micro-cap companies decline substantially. Artrya has had the added burden of its failure to secure FDA approval back in 2022.

However, as previously discussed, SCP achieving FDA approval for SCP is the largest and most significant risk hurdle (see ‘Artrya: 4Q25 results – SAPPHIRE progressing’). With the approval achieved, it now comes down to execution.

Looking ahead, the next twelve months will see Artrya achieve several other milestones that should serve as catalysts for the group’s underlying value to be better reflected in its share price, the key being:

As with any company, and especially small caps, the market will respond to performance, so depending on when AYA pulls the trigger on charging the full US$750 fee for SCP (we hope to get clarity on tomorrow’s call), we could start seeing meaningful revenue generation in the December quarter and reported in January 2026.

Download the report for the complete analysis.