Artrya submits SCP for FDA approval

Artrya announced today that it had submitted its application for approval by the FDA for its second product, Salix Coronary Plaque (SCP). The FDA aims to complete the approval process within 30 days, with the clock stopped if they request additional data. AYA is leveraging the recent (Mar-25) approval of Salix Coronary Anatomy (SCA) to streamline the process, so we expect SCP to be approved by August or September.

AYA reports that it remains on track to submit Salix Coronary Flow (SCF) for approval in 2Q26, with approval expected in early 2026. SCF attracts a US$1,017 US Medicare rebate, which should net AYA US$800 per scan.

SCP will generate ~70% of group revenue

SCP approval is a significant step for AYA. It is AYA’s main revenue-generating product, responsible for ~70% of future revenue. Importantly, it also qualifies customers for a US$950 US medicare rebate for AI-assisted coronary plaque assessment, earning hospitals ~US$200 (net of AYA fees) every time it’s used.

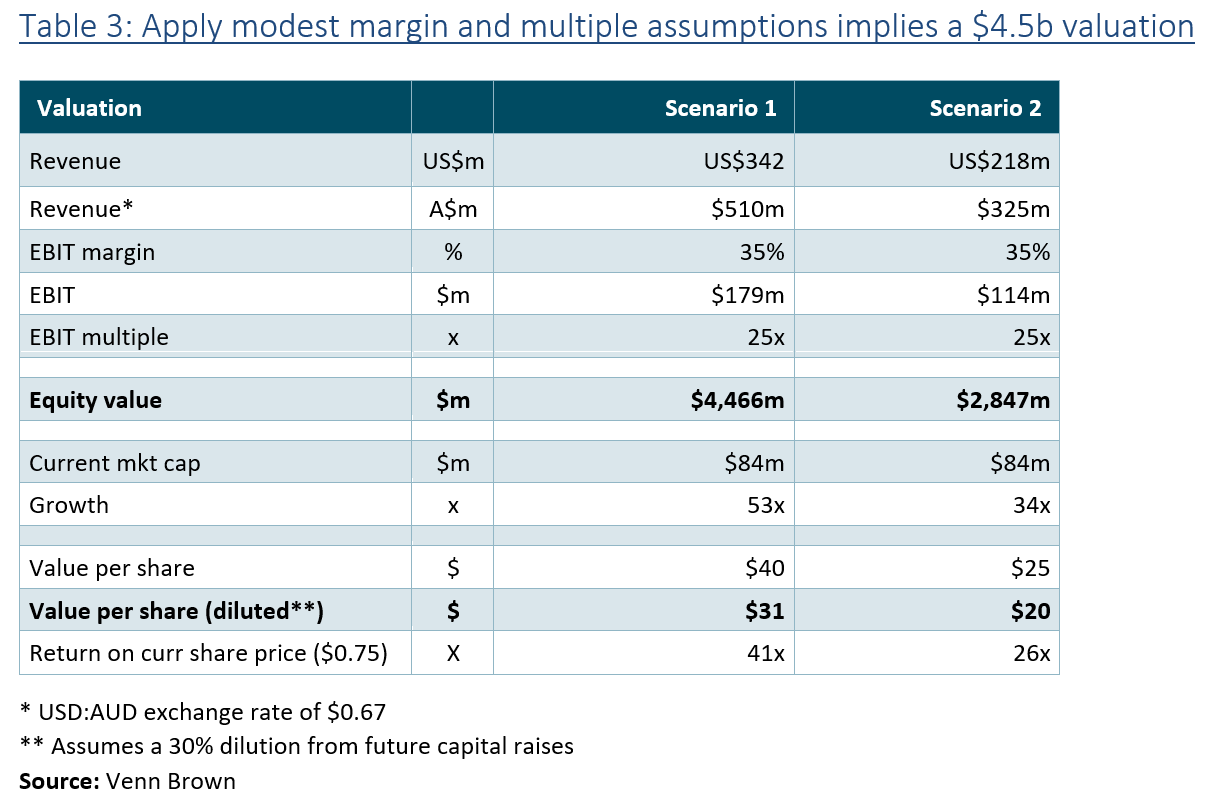

SAPPHIRE partners could add $4.5 billion of value to AYA

During its 3Q25 results call in May, AYA announced that it was in “deep discussions” with six to eight hospital groups in the US to participate in the new SAPPHIRE study (see below). Combined, these groups perform approximately 400,000 scans per year (~9% of the current US market), which equates to around US$342 million in revenue. This figure dwarfs even Venn Brown’s FY35 revenue forecast of US$213 million.

Applying a conservative EBIT margin and multiple (35% and 25x) to this revenue forecast implies an equity value of $4.5 billion, 53x the company’s current market cap ($81m). This is the equivalent to $40 per share, or $31 per diluted share (assuming 30% dilution from future capital raises), compared to the current share price of around $0.75.

It is still several years before AYA can realise this value, but the exercise demonstrates the rapid earning potential and value uplift we could see from the company. Also keep in mind, these 6-8 partners represent just 9% of the existing market, which is expected to grow at 15% per year.

Catalysts

We see several catalysts that will progressively see AYA’s share price more accurately reflect the company’s fair value, including FDA approval and launch of SCP, reporting its first US revenues, the signing of SAPPHIRE study partners, and FDA approval and launch of Salix Coronary Flow.

Read more in our initiation of coverage report: Salix: The future of cardiac imaging diagnostics.