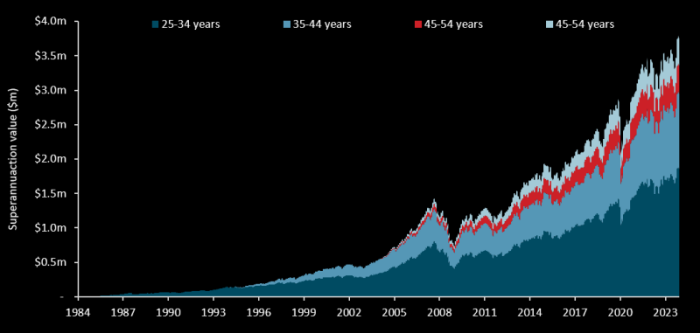

To highlight the impact of long-term investing, we calculated the retirement value of superannuation contributions made during four different decades of a person’s working life. For simplicity, we assumed a superannuation (savings) rate of 10% of a person’s annual salary. The share of returns provided by each decade are largely the same irrespective of whether the rate is 9%, 10% or 11%:

1. Ages: 25 – 34

2. Ages: 35 – 44

3. Ages: 45 – 54

4. Ages: 55 – 64

Using the current Australian average income for each age bracket, we modelled returns based on the ASX All Ordinaries Accumulation Index from March 1984 through to today (without fees). The contributions made when someone is aged 25-34 represent just 22% of their total contributions, but 40 years later, these contributions represent 62% of their total savings. Similarly, the contributions made between 45-55 represent 28% of total contributions, but only 9% of retirement savings.

As the famous quote goes “Compound interest is the eighth wonder of the world.”

The value of the contributions at retirement is determined by the time in the market rather than the size of the initial contribution, with the retirement value of later decades’ contributions progressively decreasing as a share of the total. The point is illustrated more clearly in figure below, which shows the total superannuation savings by contribution period, assuming all contributions are invested in the ASX All Ordinaries Accumulation index (without fees).

Despite earlier contributions being impacted by several downturns (1987, 1991, 2000 tech bubble), after 40 years, the contributions made between 1984 and 1994 represent 62% of total retirement savings. Meanwhile, contributions made during the traditional peak earning period (ages 45-54),representing 28% of total contributions, only generate 9% of total retirement savings.

Download the report for the complete analysis.