Artrya reported its 3Q2. With commercialisation only really starting during the quarter, income from customers remains low.

AYA continues to make progress on its Salix Coronary Flow (SCF) FDA submission. SCF is “calibrated and locked down” with AYA working to complete the clinical study, which it will include in its FDA submission.

Management has previously reported that the delay in submission (originally slated for late CY25 and then pushed to 4Q26) is due to its difficulty in obtaining sufficient high-resolution scans of patients undergoing invasive coronary angiography against which it can validate SCF.

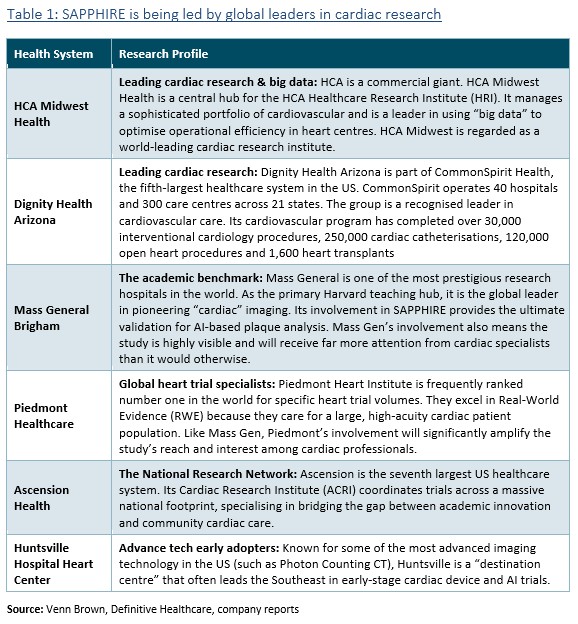

During the quarter (as previously reported – see ‘Artrya: SAPPHIRE: HCA Midwest joins the party’ and ‘Artrya: Joins the ASX All Ords. Next stop ASX 300’), two large healthcare systems joined the SAPPHIRE study: Dignity Health Arizona and HCA Midwest Health.

Commencement of the SAPPHIRE study is a major milestone and perfectly positions the company for cost-effective marketing and mass adoption over the coming several years.

Along with leading cardiac and research healthcare systems, the SAPPHIRE study now includes the 7th, 5th and largest healthcare systems in the US. We’re confident that the study now includes partners that together complete the combined 400,000 annual CCTA scans, as management initially flagged when announcing the study.

In February, AYA appointed Wesley Staggs as the new US General Manager. Staggs has a strong background in sales and commercial development, suggesting that, as well as US operations, he’ll also lead US commercialisation activity. This is a positive development and, hopefully, an indication that CEO John Konstantopoulos is delegating some of the numerous responsibilities he’s been carrying since taking over as CEO last July.

The appointment of Staggs is the second significant US hire following the appointment of Dr Jeffrey Le Benger to the board, who has a multi-decade track record of rapidly growing US medical companies and hospital groups.

AYA has not changed its earlier estimates that its foundation partners will generate approximately US$15 million in annual revenue. We don’t expect them to hit this run rate until CY27, although by that time, we believe management expects (but has not stated) to have commercial agreements with more US customers.

Tanner Health: Salix Coronary Anatomy and Salix Coronary Plaque are now rolled out to all five of Tanner’s hospitals. Management reports that the timing of payments has pushed cash recognition into 2Q26, which is why we didn’t see a step-up in cash receipts in 1Q26.

The complete rollout (which will allow broader use of the system) still requires reimbursement and back-office processes to be completed, which are now in the final stages.

Northeast Georgia Services & Cone Health: AYA reports it’s on track to have Salix rolled out to NGHS (commencing in May) and Cone (by the end of FY26), which should lead to a step-up in customer receipts from 2Q27. This is a modest delay from our expectations of more meaningful receipts commencing 1Q27.

It’s looking increasingly unlikely that AYA will be cash flow positive by FY27. We don’t see this as a negative and never assumed the group would reach this target. To be cash flow positive by FY27 requires:

Management has always stated that the three initial customers were worth US$15 million in annual revenue. To hit this revenue requires a full ramp-up in scan volumes in early FY27 in order to have a full 12 months at the targeted annual scan volume. Given that none of the foundation customers have yet been fully implemented, let alone scan volumes ramped up to the targeted volumes, we don’t see the three foundation partners providing this revenue in FY27.

Second, the time required to onboard the foundation partners highlights the complexity of integrating Salix across a hospital group, which requires approval and support from at least five departments (and probably more): administration, cardiology, imaging, IT, and billing.

We estimate the time from commercial agreement to full rollout to be 6-9 months, with a full ramp to reach target volume taking another 6-9 months. We expect these timelines to shorten as AYA’s support capability expands and becomes more experienced, but it won’t be a 3-6-month turnaround for some time.

We’re happy to be wrong, but until proven otherwise, these are the timelines we expect to see for at least the next two years. The one caveat regarding our cash flow expectations is that we don’t have any visibility into whether AYA is currently in discussions with new commercial partners.

If discussions are in advanced stages, new commercial partners could start generating cash in early CY27.

As we’ve repeatedly said, we see AYA as having a massive first-mover advantage, as the first system in the market to offer a wholly automated (human-out-of-loop) solution. As such, we believe getting Salix into more hospital groups (primarily through customer outreach and awareness of and success with SAPPHIRE) is more important than overly curtailing spending to hit an arbitrary (and meaningless in the long term) cash flow target.

Including its $30 million term deposit, AYA has $77 million in cash. Over the next 14 months, independent of customer receipts, the company will likely gain ~$34 million in additional cash:

Putting this in perspective, AYA’s last twelve months’ operating cash flow was -$16.2 million (or $23.3 million excluding interest and R&D tax rebates). At its current rate of spending, unless the group’s share price drops below $3 (for an extended time), the company will barely touch the $77 million in cash on its balance sheet. And at $5 per share, it won’t need any of its cash holdings.

AYA continues to trade below our valuation. Future catalysts include: launch of the SAPPHIRE study, lodgement of the SCF FDA application, SCF FDA clearance, and reporting its first six months of US SCP revenue in 1H27.

Artray is hosting a results call tomorrow, Friday, 1st May at 12:30 AEST: