Artrya announced on Tuesday that it has secured binding commitments for $75 million in a placement to institutional and sophisticated investors. This is well above the initially announced $60 million target (announced on the 5th September), with reports of demand being several multiples of the final figure.

Accompanying the placement is a $5 million share purchase plan open to existing shareholders (record date of 8th September), also priced at $2.05. AYA reserves the right to accept over-subscriptions. Given the current share price, we expect it will be oversubscribed. The issue price is just 6% below Thursday’s close price ($2.18), the day before the raise was announced.

Management reports it will use the funds to accelerate into the US market:

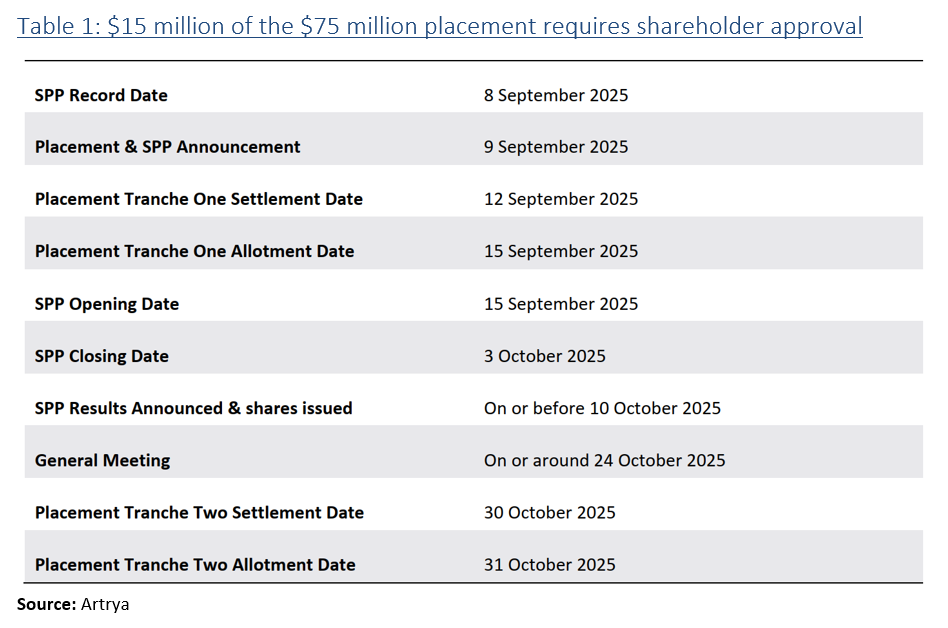

The $5 million share purchase plan open to existing shareholders is expected to open on the 15th September and close on the 3rd October (see key dates in Table 1 below).

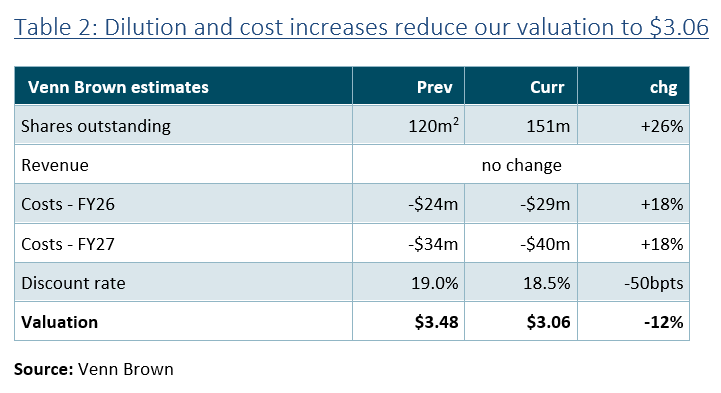

We’ve reduced our valuation to $3.06 per share (from $3.48) as a result of the significant dilution (35%) and an expected increase in costs, which is slightly offset by the cash on balance sheet and a 50 basis point reduction in discount rate given the group’s reduced capital raising and financial risk.

We will not increase our revenue expectations until we see sales traction or progress of the SAPPHIRE study, as evidenced by partners joining the study. While we believe strongly in the Salix product, management needs to demonstrate its ability to commercialise it.

(2) We had previously assumed a $15 million capital raise in mid-FY26 at $2.00 a share, adding 7.5 million shares to the current 113 million shares outstanding.

Artrya is completing the placement in two tranches (~$60 million now, ~$15 million in October), as the full $75 million exceeds the company’s current placement capacity under ASX listing rules.

Around the 24th of October, the company will hold a shareholder meeting to obtain shareholder approval for the second tranche. Once the first tranche of shares is issued, approximately 19% of the outstanding shares will be owned by insiders, and another 20% will be owned by Tranche 1 investors (totalling 39%). As such, it’s highly unlikely shareholders will reject the proposal.

However, it will be interesting to see how many shareholders cast a protest vote.

Download the report for the complete analysis.