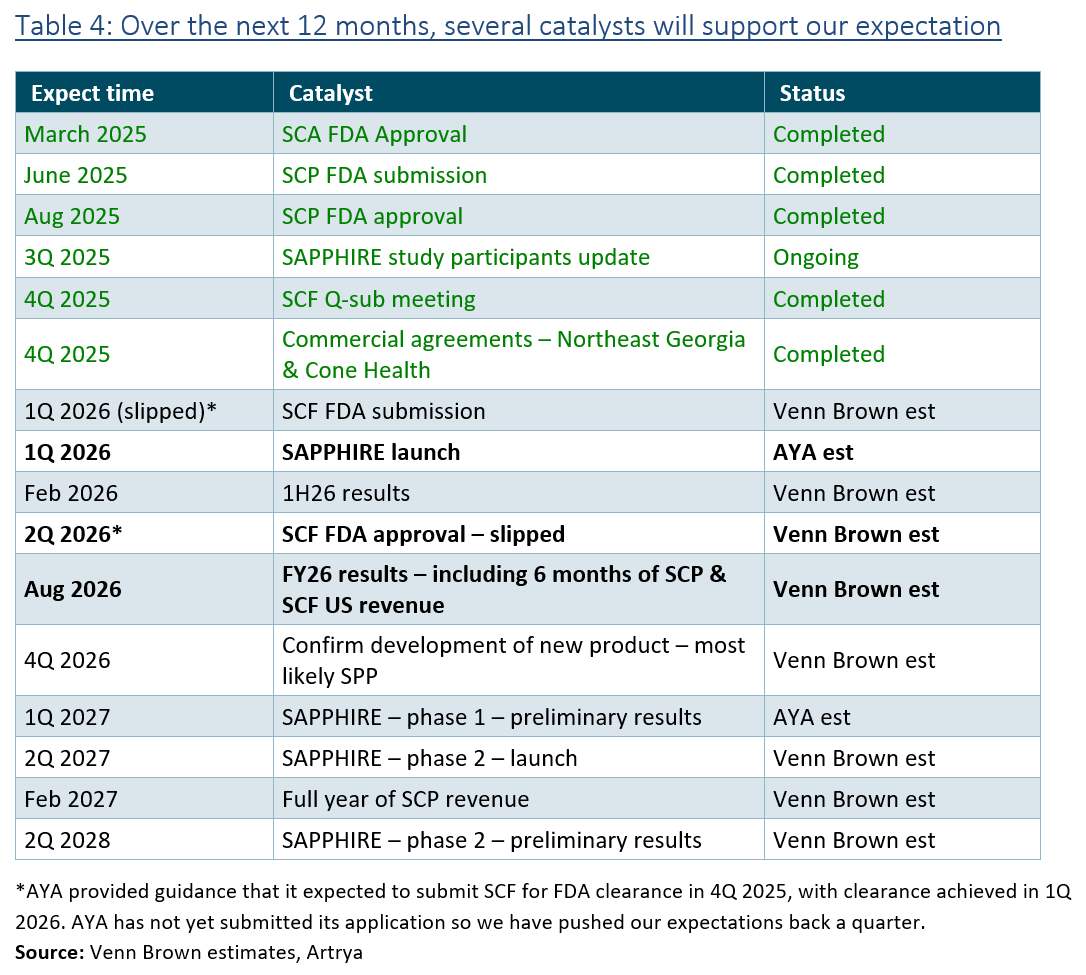

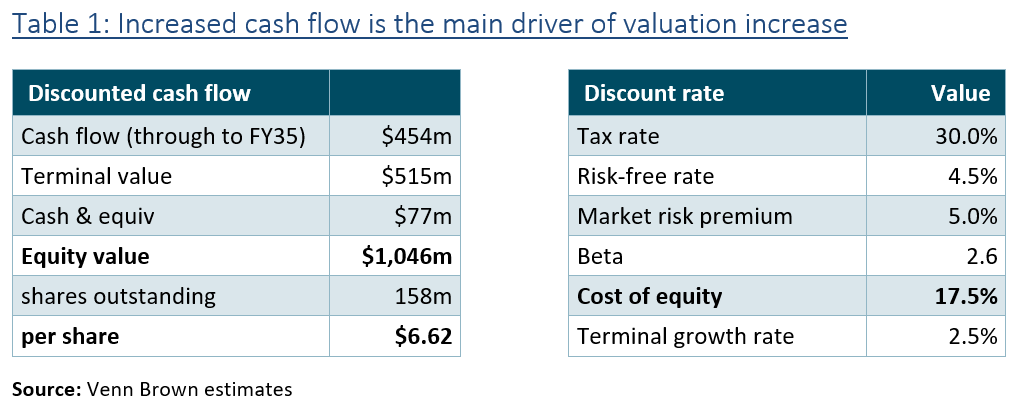

Following the events at the end of 2025 (outlined below), we’ve revised our earnings forecasts, resulting in an increase in our valuation to $6.62 per share. Apart from including the dilution impact of the capital raise, this is our first valuation review since August.

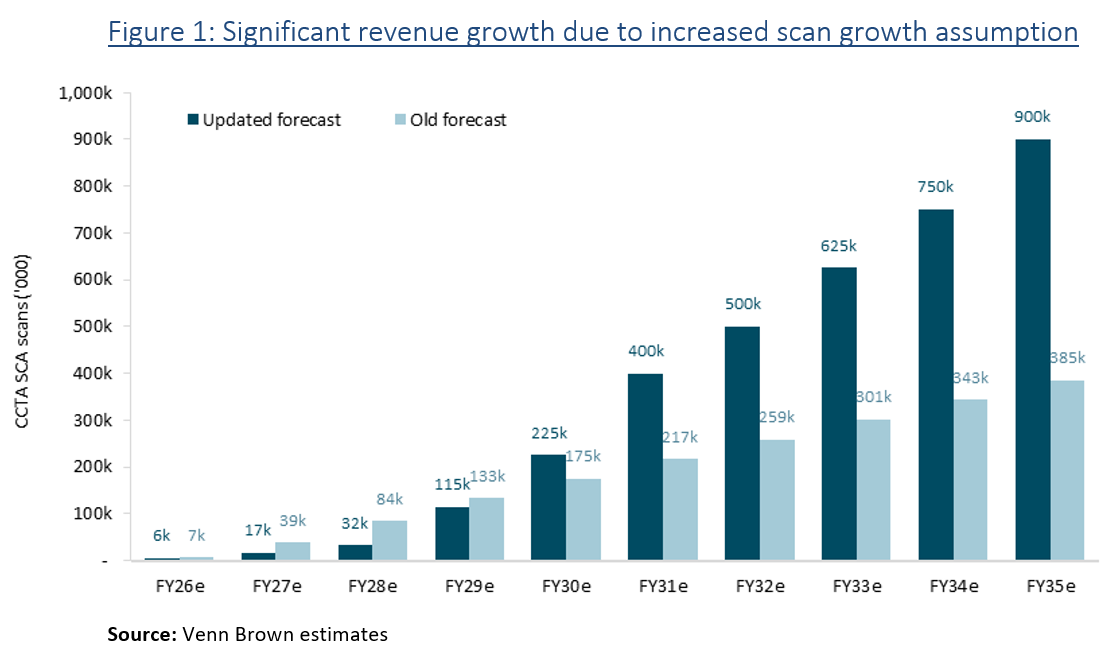

The valuation uplift is due to an increase in expected scan volumes from the commercialisation of SAPPHIRE study partners, along with leveraging the awareness and credibility generated by the study.

While the partners should be viewed as “warm leads”, the size and calibre of the partners lend enormous credibility to the study and to Salix as a diagnostic and workflow tool, with Mass General and Ascension (the seventh-largest health care system in the US) now confirmed participants (see Table 11).

AYA has confirmed four SAPPHIRE partners, which we estimate complete a combined ~200,000–250,000 CCTA scans annually. We estimate the combined volumes represent 50-60% of the targeted 400,000 annual scans for study participants. We still expect the study to commence in 1Q26, with confirmation of the remaining 2-4 study partners expected in the coming months.

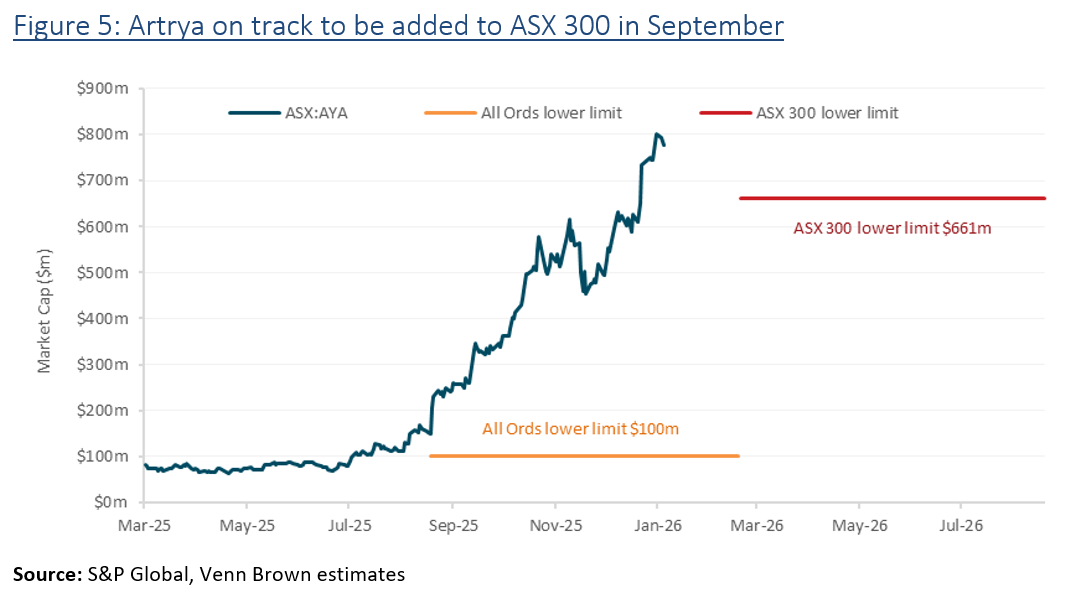

We expect AYA to be added to the All Ordinaries index at the March rebalance. Following the recent price increase, Artrya’s market capitalisation has exceeded the current level (~$660) required for inclusion in the ASX 300. The earliest rebalance AYA could qualify for is September 2026. Unless there is a significant downward change in AYA’s share price or uplift in the share price of the smallest 40 companies in the ASX 300, we expect AYA to be included in the index in September.

The end of 2025 saw a flurry of activity setting 2026 up as a year of significant growth and development: AYA was added to the S&P/ASX All Technologies Index, commercial agreements were signed with AYA’s remaining two foundation partners, and confirmation of two significant SAPPHIRE partners.